Under the Hart-Scott-Rodino Act, both the U.S. Department of Justice and the Federal Trade Commission have authority not only to review most proposed mergers and acquisitions that take place in the United States for possible antitrust concerns, but to halt such a proposed transaction if they believe that the deal would “substantially lessen competition.” Both agencies, however, may also approve a particular merger or acquisition on the condition that the acquiring or acquired entity divest itself of certain businesses or operations.

In the latest example of this conditional-approval authority, on May 25 the Justice Department announced that it had reached agreement with Huntington Bancshares Incorporated and TCF Financial Corporation to have the companies sell 13 branches in the state of Michigan (with approximately $872.3 million in deposits), to resolve antitrust concerns arising from Huntington’s planned acquisition of TCF Bank. The divested assets include all of the deposits and loans associated with the 13 divested branches, as well as the physical assets.

Key provisions of the financial institutions’ agreement with the Justice Department include:

- Divestiture of the 13 branches in 9 counties and the City of Midland;

- The companies’ agreement “to suspend existing, and not to enter into new, non-compete agreements with branch managers and loan officers located in the divestiture counties for a period of 180 days following the consummation of their merger”;

- The companies’ agreement that any traditional branches that are located in any overlap market in Michigan and Ohio and that are closed within three years of the merger’s closing “will be sold or leased to an insured depository institution that offers deposit and credit services to small businesses.”

As a result of the acquisition, Huntington, which currently has approximately $120 billion in assets, will become the 25th largest bank holding company based on assets.

It should be noted that the 13 branches to be divested represent a vanishingly small percentage of the total number of branches that Huntington and TCF have. Currently, Huntington has 839 full-service branches across seven Midwestern states, and TCF has 475 branches primarily located in Michigan, Illinois, and Minnesota. The 13 branches therefore represent less than one percent of the total number of Huntington and TCF branches.

On its face, the divestiture of so small a number of bank branches would not seem to make much of a difference in avoiding the “substantia[l] lessen[ing of] competition.” In this case, however, the Federal Reserve Board, noted – after analyzing such competitive factors as the number and strength of competitors that would remain in the relevant markets and the current and expected increased concentration levels of market deposits — that the divestitures that Huntington and TCF proposed in four banking markets are “significant” and “ensure that the proposed transaction will present no competitive concerns under the [Bank Holding Company] Act or Section 7 of the Clayton Act.”

While the transaction still requires final approval by the Board, the Justice Department has advised the Board that the Department

“will not challenge the merger provided that the parties divest branches in certain areas of overlap and agree that any traditional branches in Michigan and in the five overlapping counties in Ohio that are closed within three years following the merger, will be marketed to an institution with a demonstrated record of providing services and loans to the local community.”

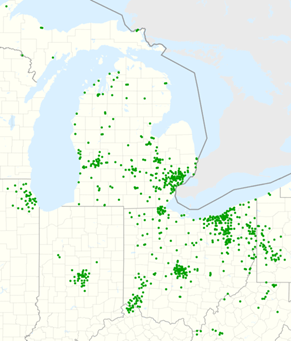

Figure: Geographic Footprint of Huntington Bancshares Branches (As Of February 13, 2021) [Public Domain]